In the previous post, the Average True Range (ATR) indicator was introduced as a practical tool for managing and defining risk. In this section, the focus shifts toward another equally critical function of ATR: its ability to measure market volatility with clarity and consistency.

Average True Range is a widely used technical indicator that is typically plotted at the bottom of a price chart. Its configuration is straightforward, requiring only a single input parameter—the number of periods used for calculation. The standard setting is 14 periods, which provides a balanced view of recent market activity. However, traders retain full flexibility to adjust this parameter, allowing for either a shorter-term sensitivity or a broader, long-term perspective depending on their trading objectives and strategy.

Importantly, ATR values are expressed in the same price format as the underlying asset. For example, when analyzing EUR/USD, an ATR reading of 0.0048 corresponds to 48 pips over the selected lookback period. If market conditions become more volatile, this value will expand accordingly. A reading of 0.0080, for instance, reflects an average movement of 80 pips. This direct translation into price movement makes ATR particularly effective for quantifying real market activity.

An increase in volatility, as reflected by a rising ATR, provides actionable insight for traders. Higher volatility may signal opportunities for strategies that thrive on larger price swings, while lower volatility may favor range-bound or mean-reversion approaches. In some cases, elevated volatility may also serve as a warning to avoid market participation altogether if conditions exceed a trader’s predefined risk tolerance. As established in volatility-focused trading frameworks, aligning strategy selection with prevailing market conditions is essential, and ATR offers a reliable mechanism for monitoring this dynamic variable.

The daily chart of EUR/USD below illustrates how shifts in volatility are captured through the ATR indicator over time.

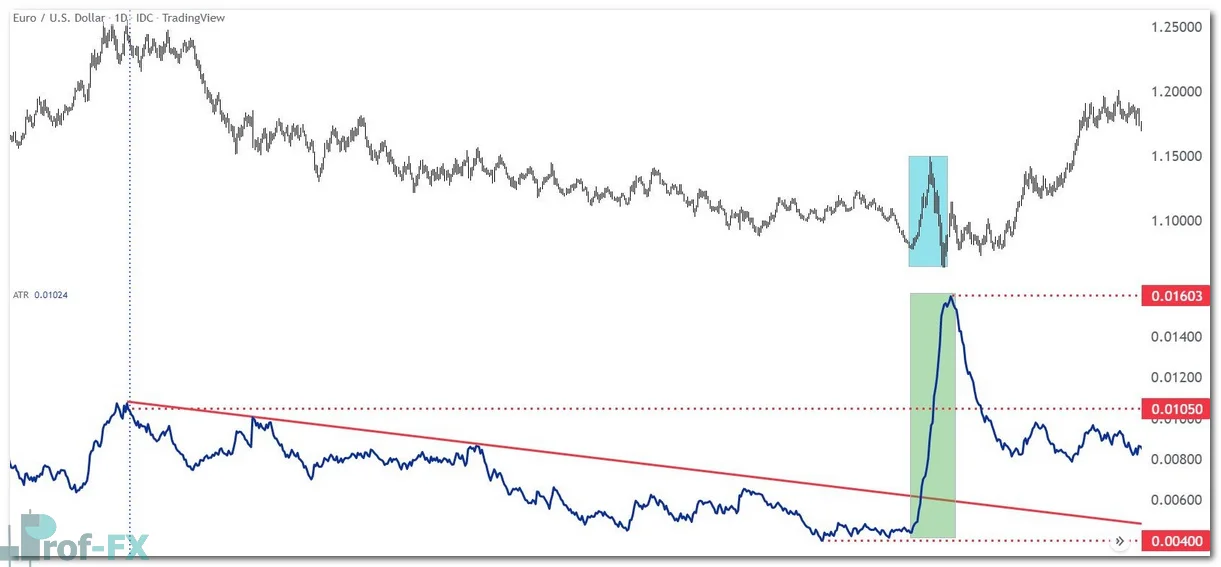

During the early part of 2018, ATR readings were near 105 pips, indicating that the average daily price range over the prior 14 periods was approximately 105 pips. As EUR/USD continued within a sustained bearish trend throughout 2018 and into 2019, volatility gradually declined. By the end of 2019, ATR had decreased to around 40 pips, reflecting a significantly calmer market environment.

However, this stability changed dramatically in early 2020 as global uncertainty related to the COVID-19 pandemic began to influence financial markets. During this period, ATR surged sharply, eventually exceeding 160 pips by late March. This rapid expansion clearly demonstrates how heightened uncertainty and aggressive price movements are directly incorporated into the indicator’s readings.

For traders utilizing ATR to determine stop loss placement, this adaptability is particularly valuable. As volatility increases, wider stop levels may be required to accommodate larger price fluctuations, while tighter stops may be more appropriate during calmer market phases. In this way, ATR allows trading decisions to remain aligned with real-time market dynamics rather than static assumptions.

EUR/USD Daily Price Chart with ATR Applied

Average True Range is Directionally Independent

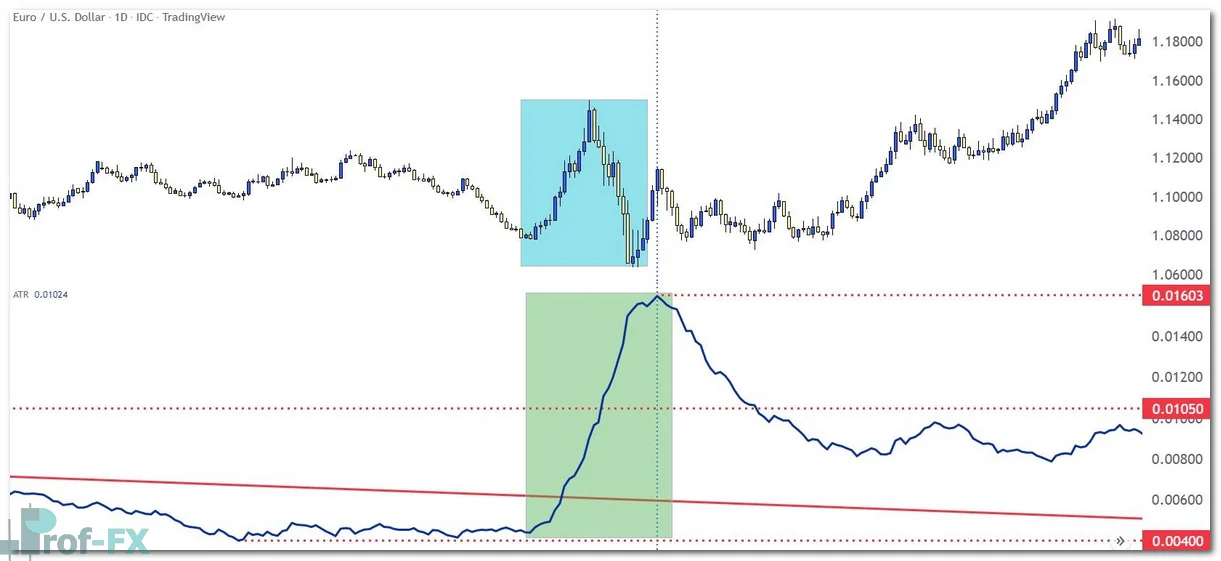

A critical characteristic of ATR, as demonstrated in the previous example, is its directional neutrality. ATR does not indicate whether the market is trending bullish or bearish; instead, it strictly measures the magnitude of price movement. This distinction is essential for proper interpretation.

The period during which the COVID-19 pandemic was being priced into the market provides a clear illustration. Even as EUR/USD shifted direction during this time, ATR continued to rise. This confirms that the indicator responds solely to the intensity of price fluctuations, not the direction in which prices are moving.

Further analysis of the chart shows that ATR reached its peak on March 27, 2020. This peak coincided with the point at which the most extreme price movements began to subside following the highly volatile trading conditions observed in late February and early March. As the magnitude of price swings decreased, ATR gradually declined, reflecting a normalization of market volatility.

This behavior reinforces a key conclusion: ATR is a pure volatility metric. It enables traders to objectively assess how much the market is moving, without introducing directional bias. As a result, ATR serves as a foundational component in risk management, position sizing, and strategy selection, ensuring that trading decisions are consistently aligned with prevailing market conditions.

EUR/USD Daily Price Chart

{kind=link}