Implied volatility, often abbreviated as IV and also referred to as expected volatility, represents a key variable used to estimate the magnitude of price movements in a specific market or financial instrument. It quantifies the anticipated size of fluctuations in an underlying asset, making it a critical metric for evaluating market expectations.

From an analytical standpoint, implied volatility does not indicate price direction, whether bullish or bearish, but instead reflects how significant price movements are expected to be within a given time horizon.

What Is Implied Volatility?

Implied volatility is expressed as a percentage and reflects the level of uncertainty or perceived risk among market participants. It is derived from the Black-Scholes options pricing model, which calculates theoretical option values based on multiple inputs, including IV.

This metric provides insight into the expected variability of assets such as equity indices, stocks, commodities, and major currency pairs over a defined period.

Because implied volatility directly influences option pricing, it is a core variable closely monitored by options traders. However, its relevance extends beyond the options market. Many traders and analysts incorporate IV into broader trading strategies due to the valuable information it provides regarding market conditions.

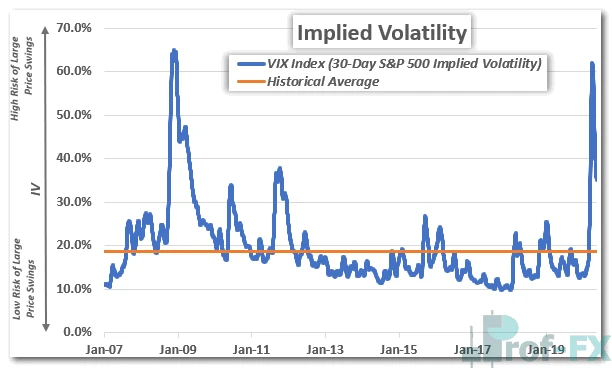

A widely recognized example is the VIX Index, which represents the 30-day implied volatility of at-the-money S&P 500 options. It is commonly used as a benchmark for measuring overall market risk.

A higher VIX level, or elevated implied volatility, indicates increased uncertainty and a higher probability of substantial price fluctuations. This expanded range of potential outcomes results in higher option premiums. Importantly, this positive relationship between implied volatility and option prices applies equally to both call options and put options, assuming all other variables remain constant.

Beyond pricing, implied volatility serves multiple analytical purposes, including:

- Comparing implied volatility with realized (historical) volatility

- Assessing overall market sentiment

- Identifying potential support and resistance levels

- Evaluating cross-asset relationships

These applications establish implied volatility as a multi-dimensional tool in professional trading analysis.

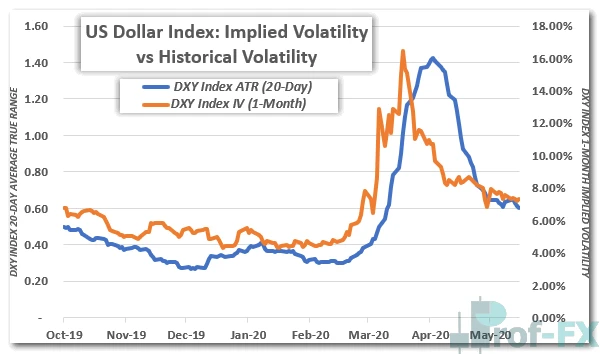

Implied Volatility vs Historical Volatility

Implied volatility reflects expectations about future price movements, while historical volatility, also known as realized volatility, measures past price fluctuations that have already occurred.

For example, indicators such as the Average True Range (ATR) quantify historical volatility by illustrating the average price movement over a specific period.

Although these two metrics differ in their forward-looking versus backward-looking nature, they are closely related and often exhibit similar behavioral patterns. Periods of high uncertainty, such as major economic data releases or central bank decisions, tend to drive higher implied volatility. These conditions frequently lead to increased realized volatility as market activity intensifies.

Conversely, during stable market environments characterized by low risk perception, both implied and historical volatility tend to remain subdued.

This relationship confirms that implied volatility is not arbitrary, it is deeply rooted in observable market dynamics.

Implied Volatility as a Measure of Market Risk

Implied volatility functions as a projection of expected market movement, independent of direction. It defines the probable range within which an asset’s price may fluctuate and reflects the degree of uncertainty surrounding that movement.

High implied volatility signals that traders anticipate larger price swings, while low implied volatility indicates expectations of relatively stable price action.

As such, IV serves as a reliable proxy for market sentiment. Elevated readings typically correspond to heightened fear or uncertainty, whereas lower readings suggest confidence and stability within the market.

This makes implied volatility a crucial indicator for assessing overall market risk.

Using Implied Volatility to Identify Support and Resistance

Implied volatility can also be integrated into technical analysis frameworks. One of its practical applications is defining potential support and resistance levels through implied trading ranges.

These ranges are commonly calculated based on a one standard deviation assumption, which implies a 68% probability that price will remain within a defined range over a specified period.

Statistically:

- If price reaches the upper boundary, there is an 84% probability it will move lower and a 16% probability it will continue rising.

- If price reaches the lower boundary, there is an 84% probability it will move higher and a 16% probability it will continue falling.

This probabilistic framework provides traders with a structured method to anticipate potential reversal zones or continuation scenarios.

Advantages of Implied Volatility in Forex Trading

In the forex market, implied volatility is particularly effective due to the mean-reverting nature of major currency pairs. This characteristic enhances the reliability of implied volatility trading ranges as actionable signals.

For instance, consider a EUR/GBP scenario where:

- Spot price: 0.8541

- Implied volatility: 7.3% (1-day option)

Using these inputs, the estimated 24-hour trading range was:

- Implied support: 0.8508

- Implied resistance: 0.8574

This calculation suggested a one standard deviation move of ±0.0033, equivalent to a 66-pip range around the spot price.

As the market evolved, EUR/GBP reached an intraday high of 0.8578 but failed to sustain momentum, eventually closing lower at 0.8547. This price action followed a rejection at the implied resistance level, reinforcing the validity of IV-based technical boundaries.

This example demonstrates that implied volatility can effectively highlight potential inflection points, enabling traders to identify high-probability trading opportunities.

Applying Implied Volatility Across Markets

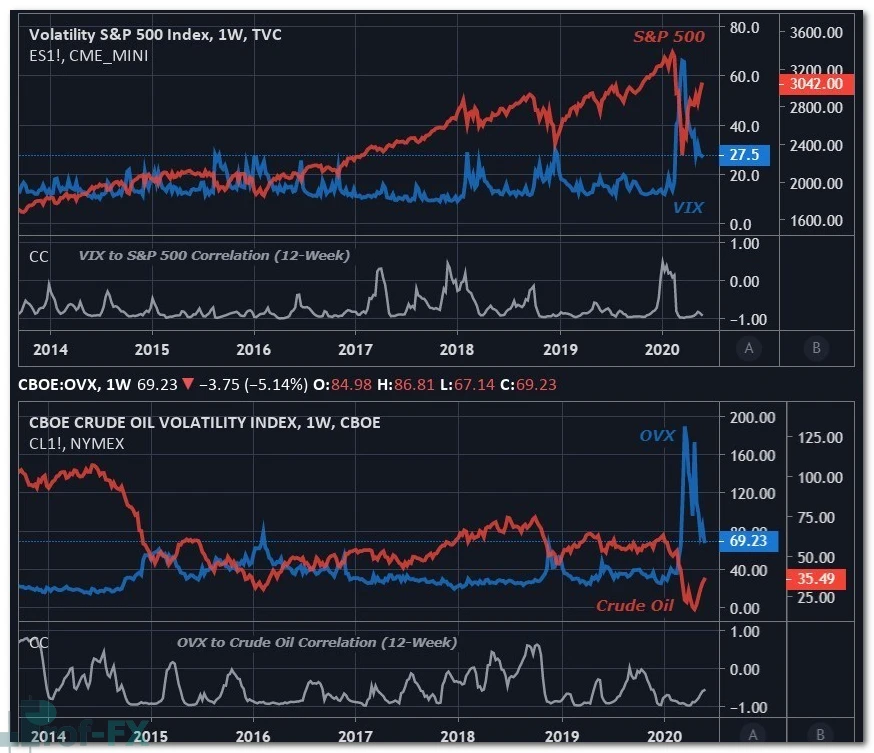

Implied volatility is not limited to forex; it is equally applicable to commodities, stocks, and indices. It provides a macro-level view of market uncertainty and helps identify relationships across different asset classes.

One of the most prominent benchmarks is the S&P 500 VIX Index, often referred to as the “fear gauge.” The VIX typically rises during periods of market stress and declining equity prices, maintaining a strong inverse relationship with the S&P 500.

Similarly, the OVX Index, which tracks expected volatility in crude oil prices, reflects sentiment in energy markets. Given that crude oil and equities often respond similarly to changes in risk appetite, both tend to show negative correlations with volatility indices during risk-off environments.

While inverse relationships between price and implied volatility are common, they are not universal. Correlations are dynamic and may strengthen or weaken depending on prevailing market conditions.

In contrast, certain safe-haven assets can exhibit a positive relationship between price and volatility. For example:

- The US Dollar Index (DXY) often aligns with currency volatility (FXVIX)

- Gold prices frequently show positive correlation with gold volatility (GVZ)

These variations underscore the importance of context when interpreting implied volatility data.

Conclusion

Implied volatility is a foundational metric that provides insight into expected market movement, perceived risk, and trader sentiment. Its influence on option pricing, combined with its ability to define probabilistic trading ranges and cross-asset relationships, makes it an indispensable tool in modern trading.

From a professional standpoint, integrating implied volatility into trading strategies is not optional, it is essential for achieving a comprehensive and data-driven understanding of market behavior.

Prof FX delivers forex news and technical analysis focused on the key trends shaping global currency markets.

{kind=link}