Contractionary monetary policy is one of the most powerful tools used by central banks to control inflation and prevent economies from overheating. While the concept may sound counterintuitive – intentionally slowing economic activity – it plays a critical role in maintaining long-term economic stability and financial credibility.

This article explains what contractionary monetary policy is, how it works, the tools central banks use, and its real-world effects, presented in a clear and practical way for traders, investors, and market observers.

What Is Contractionary Monetary Policy?

Contractionary monetary policy refers to a set of actions taken by a central bank to reduce inflation and slow excessive economic growth. Policymakers achieve this by tightening financial conditions through a combination of:

- Raising interest rates

- Increasing reserve requirements for commercial banks

- Reducing the money supply via large-scale bond sales, commonly known as quantitative tightening (QT)

Although slowing economic activity may appear undesirable, an economy operating above its sustainable capacity often generates harmful side effects—most notably inflation, which erodes purchasing power and distorts long-term investment decisions.

The challenge for central banks is to reduce inflation without triggering a recession. This careful balancing act is frequently described as achieving a “soft landing”, where borrowing becomes more expensive, spending moderates, and inflation cools – while employment and growth remain intact.

From Accommodative to Contractionary Policy

Contractionary policy typically follows a prolonged period of accommodative (supportive) monetary policy. During accommodative phases—often after recessions—central banks:

- Lower benchmark interest rates

- Inject liquidity into the economy through quantitative easing (QE)

When interest rates approach zero, borrowing costs fall dramatically, encouraging consumption, investment, and risk-taking. Over time, however, excessive stimulus can fuel inflation, asset bubbles, and financial imbalances. At that point, central banks pivot toward contractionary measures to restore equilibrium.

Key Tools of Contractionary Monetary Policy

Central banks rely on three primary mechanisms to tighten financial conditions. Each tool affects the economy through a different transmission channel.

1. Raising the Benchmark Interest Rate

The benchmark interest rate—often referred to as the base or policy rate—is the interest rate at which a central bank lends money to commercial banks on an overnight basis. This rate serves as the anchor for the entire interest rate structure within an economy, influencing everything from short-term money market rates to long-term borrowing costs faced by consumers and businesses.

When a central bank raises the benchmark interest rate, the impact spreads quickly across the financial system.

Commercial banks pass higher funding costs on to borrowers, leading to increases in mortgage rates, personal loan rates, credit card interest, and business lending rates. As a result, the cost of borrowing rises broadly throughout the economy.

Debt servicing costs increase for both households and corporations.

Higher interest rates mean that existing variable-rate loans become more expensive, while new debt is issued at less favorable terms. For households, this often translates into higher monthly mortgage and loan payments. For businesses, higher interest expenses reduce cash flow and profitability, forcing management teams to reassess spending priorities and expansion plans.

Disposable income declines as a larger share of earnings is allocated to debt repayments.

When households dedicate more income to servicing debt, they have less available for discretionary spending. Similarly, businesses facing higher financing costs may delay hiring, cut back on capital expenditures, or postpone strategic investments.

As borrowing becomes more expensive, both households and businesses naturally reduce spending and investment, leading to a moderation in overall economic activity. This slowdown in demand is precisely the mechanism through which higher interest rates help ease inflationary pressures. By curbing excessive consumption and speculative investment, central banks aim to restore price stability while avoiding severe disruptions to economic growth.

For traders and investors, changes in the benchmark interest rate are among the most closely watched policy decisions, as they directly influence currency valuations, bond yields, equity markets, and broader financial conditions.

2. Raising Reserve Requirements

Commercial banks are required to hold a specified portion of customer deposits as reserves at the central bank rather than lending those funds out. These reserves serve two critical purposes: they ensure that banks have sufficient liquidity to meet withdrawal demands during periods of financial stress, and they provide central banks with a powerful mechanism for regulating the supply of money and credit within the economy.

When a central bank raises reserve requirements, it directly reduces the amount of money banks are able to lend.

A higher reserve ratio means a larger share of deposits must remain idle at the central bank, leaving banks with less capital available to extend loans to households and businesses. Even if demand for borrowing remains strong, banks may be unable to meet it due to these tighter regulatory constraints.

Credit creation slows as banks are forced to become more selective in their lending practices.

With fewer funds available, banks typically prioritize lower-risk borrowers, raise lending standards, or reduce loan volumes altogether. This results in fewer mortgages, business loans, and consumer credit being issued, which in turn dampens spending and investment across the economy.

The overall circulation of money in the economy declines.

Because bank lending is a key driver of money creation, restricting lending activity leads to a slowdown in the velocity of money—how frequently money changes hands in economic transactions. Lower money circulation contributes to reduced demand for goods and services, easing upward pressure on prices.

Raising reserve requirements is a particularly direct and forceful contractionary tool, as it limits lending regardless of prevailing interest rates. When combined with higher benchmark rates, the effects are amplified: borrowing becomes more expensive and less accessible at the same time. Together, these measures significantly tighten financial conditions, slow economic growth, and help central banks bring inflation under control.

Due to its strength and potential to disrupt credit markets, this policy tool is used sparingly in many developed economies. However, when deployed, it sends a strong signal that policymakers are committed to restraining excessive credit expansion and restoring economic balance.

3. Open Market Operations: Mass Bond Sales (Quantitative Tightening)

Another key tool central banks use to implement contractionary monetary policy is open market operations, specifically through the large-scale sale of government securities—commonly referred to as quantitative tightening (QT). This process reverses the effects of quantitative easing, during which central banks previously injected liquidity into the financial system by purchasing bonds.

When a central bank sells large quantities of government securities into the open market, it directly withdraws liquidity from the financial system. Using U.S. Treasuries as an example helps illustrate the mechanics, though the principles apply globally.

Investors must pay cash to purchase these bonds, transferring funds from private hands to the central bank. Unlike private-sector transactions, this cash is not immediately recycled back into the economy. Instead, it is effectively removed from circulation for the duration of the bond’s life, reducing the amount of money available for lending, investment, and consumption.

As liquidity tightens, financial conditions become more restrictive.

With less cash flowing through the system, banks, institutions, and investors have fewer resources to deploy elsewhere. This can dampen risk-taking behavior, slow credit expansion, and reduce demand for assets such as equities, real estate, and corporate bonds.

Bond sales also affect pricing and yields.

An increase in bond supply places downward pressure on bond prices. Since bond prices and yields move inversely, falling prices result in higher yields. Rising yields raise borrowing costs across the economy, as government bond yields serve as benchmark rates for a wide range of financial products, including mortgages, corporate debt, and long-term loans.

Higher government borrowing costs have broader fiscal implications.

As yields rise, it becomes more expensive for governments to finance deficits and roll over existing debt. This often forces policymakers to rein in discretionary spending or delay large-scale public projects, further contributing to a slowdown in economic activity.

In combination, these effects make quantitative tightening a powerful contractionary force. By simultaneously reducing liquidity, raising yields, and increasing borrowing costs, mass bond sales reinforce the impact of higher interest rates and tighter credit conditions—helping central banks curb inflation while deliberately cooling economic momentum.

The Economic Effects of Contractionary Monetary Policy

Contractionary policy influences the economy through several key channels.

1. Impact of Higher Interest Rates

Higher interest rates are the most visible and commonly used tool in contractionary monetary policy, and their effects ripple through the economy in multiple stages.

Higher interest rates discourage borrowing.

As central banks raise benchmark interest rates, borrowing costs increase across the financial system. Loans for homes, vehicles, education, and business expansion become more expensive, prompting both households and corporations to think twice before taking on new debt. This reduction in borrowing demand directly slows the pace of economic activity.

Capital investment tends to slow.

For businesses, higher interest rates raise the cost of financing long-term projects such as factory expansion, technology upgrades, or infrastructure development. Projects that once appeared profitable under low-rate conditions may no longer meet return thresholds, leading firms to delay or cancel investment plans. Over time, this results in slower productivity growth and reduced economic momentum.

Mortgage and loan payments increase for households.

Existing variable-rate loans and newly issued debt reflect higher interest costs, placing additional strain on household budgets. As mortgage payments, credit card interest, and personal loan expenses rise, consumers are left with less disposable income to spend on discretionary goods and services.

As a result, households reduce consumption while businesses adopt a more cautious approach to expansion and hiring. Together, these behavioral shifts contribute to a slowdown in aggregate demand, which is the intended outcome when central banks seek to curb inflationary pressures.

In addition, higher interest rates raise the opportunity cost of spending. When returns on savings accounts, government bonds, and other interest-bearing investments increase, individuals and institutions are incentivized to save rather than spend. This further suppresses demand and reinforces the contractionary effect of monetary tightening.

However, inflation must always be taken into account when evaluating the effectiveness of higher interest rates. If inflation remains above nominal interest rates, savers may still experience negative real returns despite higher yields. In such environments, central banks may need to maintain restrictive policy for an extended period to ensure that real interest rates turn positive and inflation expectations are brought firmly under control.

2. Impact of Higher Reserve Requirements

Raising reserve requirements is a powerful, though less frequently used, contractionary monetary policy tool. When a central bank mandates that commercial banks hold a larger percentage of customer deposits as reserves, it directly limits the amount of capital banks can lend into the economy.

When banks are required to hold more reserves, fewer loans are issued.

Capital that would otherwise be available for lending must remain idle on bank balance sheets. This reduces the flow of credit to households and businesses, affecting everything from consumer loans and mortgages to business expansion financing. As lending activity slows, the velocity of money in the economy declines.

Credit availability tightens across the financial system.

With fewer loans being approved, borrowers face stricter lending standards and reduced access to financing. Banks become more selective, favoring low-risk borrowers while marginal borrowers are often priced out of the credit market entirely. This tightening of credit conditions can weigh heavily on small businesses and consumers who rely on financing to sustain spending and investment.

Economic activity slows as a result.

Reduced lending leads to lower consumer spending, slower business investment, and fewer large-scale capital projects. Over time, this slowdown helps relieve inflationary pressures by dampening demand for goods, services, and labor.

This contractionary effect becomes especially potent when higher reserve requirements are paired with rising interest rates. Higher interest rates reduce the demand for credit by making borrowing more expensive, while higher reserve requirements restrict the supply of credit by limiting how much banks can lend. Together, these forces create a dual tightening mechanism that significantly slows economic momentum and reinforces the central bank’s efforts to bring inflation under control.

From a market perspective, this combination often signals a more aggressive policy stance, which can have meaningful implications for currency valuation, bond yields, and broader financial conditions.

3. Impact of Bond Sales and Rising Yields

U.S. Treasuries come in various maturities:

- T-bills: 4 weeks to 1 year

- Notes: 2 to 10 years

- Bonds: 20 to 30 years

Treasury yields are widely viewed as risk-free benchmarks. When bond yields rise due to mass sales:

- Government borrowing becomes more expensive

- Long-term interest rates across the economy rise

- Fiscal authorities may reduce discretionary spending

This reinforces the contractionary impulse across both monetary and fiscal channels.

Real-World Examples of Contractionary Monetary Policy

While contractionary policy is straightforward in theory, it is far more complex in practice. Central banks must navigate external shocks, geopolitical events, and structural weaknesses within the financial system. As a result, policymakers often adopt a data-dependent and flexible approach.

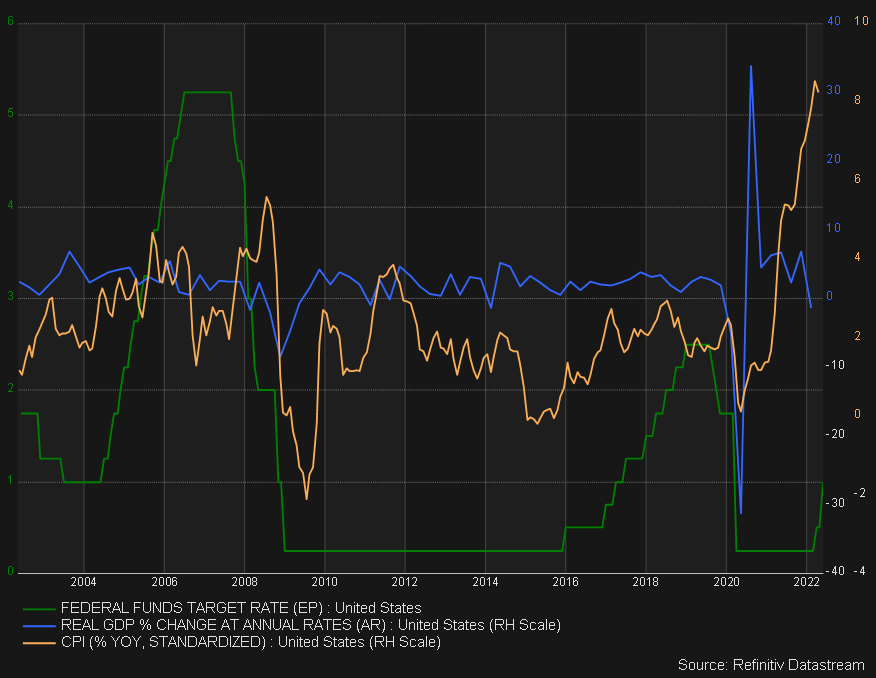

The chart below illustrates U.S. contractionary policy episodes by comparing:

- The Federal Funds Rate

- Inflation (CPI)

- Real GDP

over a 20-year period.

Key Observations from Past Contractionary Cycles

Two critical insights emerge when examining historical periods of contractionary monetary policy, particularly in the United States.

First, inflation tends to lag behind interest rate hikes.

Monetary policy does not impact the economy immediately. When central banks raise interest rates, the effects must first work their way through multiple layers of the financial system. Higher policy rates translate into higher borrowing costs for banks, which are then passed on to households and businesses in the form of more expensive loans, mortgages, and credit. This process takes time. As a result, consumer spending, corporate investment, and hiring decisions adjust gradually rather than instantly. For this reason, inflation often continues to rise—or remains elevated—for months or even years after the initial rate hikes begin.

Second, inflation continued to rise during portions of both tightening cycles before eventually turning lower.

During the 2004–2006 rate-hiking cycle and again during the 2015–2018 period, inflation did not respond immediately to higher interest rates. Instead, inflation pressures persisted as momentum from prior economic expansion and accommodative financial conditions continued to support demand. Only after sustained tightening did inflation begin to cool, reinforcing the idea that central banks must act preemptively and patiently when fighting inflation rather than expecting rapid results.

In both historical examples, contractionary monetary policy was ultimately cut short by major external crises.

- The Global Financial Crisis (2008–2009) exposed deep structural weaknesses in the financial system, forcing central banks to rapidly abandon tightening efforts in favor of aggressive emergency stimulus measures.

- The COVID-19 pandemic (2020) triggered an unprecedented global economic shutdown, compelling central banks to slash interest rates back to near-zero levels and reintroduce large-scale quantitative easing to stabilize markets and support economic activity.

These events highlight an important reality: monetary policy does not operate in a vacuum. Even well-executed contractionary strategies can be derailed by unexpected shocks. Central banks must remain adaptable, ready to reverse course when financial stability or economic survival is at risk. For market participants, this underscores why long-term policy paths are rarely linear and why flexibility and risk management are essential when navigating monetary cycles.

Final Perspective: The Limits of Monetary Policy

Contractionary monetary policy is one of the most challenging responsibilities faced by central banks. It must be implemented with precision, flexibility, and constant reassessment.

Monetary policy does not operate in isolation. External shocks—financial crises, pandemics, geopolitical disruptions—can overwhelm even the most carefully designed strategies. A useful analogy is the difference between flying in a simulator versus piloting an aircraft in severe crosswinds.

For traders and investors, understanding contractionary monetary policy is essential. Interest rate decisions, bond yields, and liquidity conditions directly influence currency markets, equities, commodities, and risk sentiment. Recognizing where the economy sits in the monetary cycle provides valuable context for navigating global financial markets.

Prof FX provides in-depth forex news and macroeconomic analysis covering the monetary policies that shape global currency markets.

{kind=link}